Whether you’ve been working for 40 years or if you’ve just entered the job market, saving for retirement is vital to your future planning. According to CNN Money, you should try to save between 10 and 15 percent of your salary starting in your 20s to have enough money to sustain you during retirement. While they make sure to point out that this is just a general guideline, saving that much money can be a daunting task – especially if you’re one of the 78% of Americans who live paycheck to paycheck.

But there’s good news!

Even if you haven’t been able to save much so far, you can always start now – and there are all kinds of options available to help you do it.

Traditional and Roth IRAs

Individual Retirement Accounts (IRAs) are an excellent option for many folks looking to save for retirement, and many of them will even allow folks age 50 and older to contribute an additional $1,000 each year.

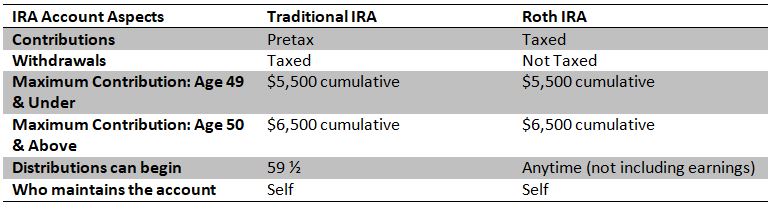

But what’s the difference between them? We’ve created a chart to help you tell them apart:

Each style of IRA has its own benefits and drawbacks, so it’s important to do your research and talk to a professional before making a decision.

Questions To Ask Before You Open an IRA

- What fees are associated?

- What times of investments are held in the account?

- Are there trading costs? How much are they?

- When do I want to be able to begin getting distributions?

- Are there penalties for early withdrawals?

Want to find out more? Reach out to us and we can help answer your questions or direct you to one of our trusted financial planning partners for more help.